Introduction

When purchasing car insurance in the United States, drivers often face an important decision: choosing between full coverage car insurance and liability insurance. Both types of policies provide financial protection, but they differ significantly in what they cover and how much they cost. Understanding the differences between these two options is essential for making an informed decision that protects your vehicle, your finances, and your legal responsibilities as a driver. While liability insurance is the minimum requirement in most states, full coverage insurance offers broader protection that includes damage to your own vehicle as well. In this guide, we will explain what each type of insurance includes, their benefits, costs, and which option may be best for different types of drivers.

What Is Liability Car Insurance?

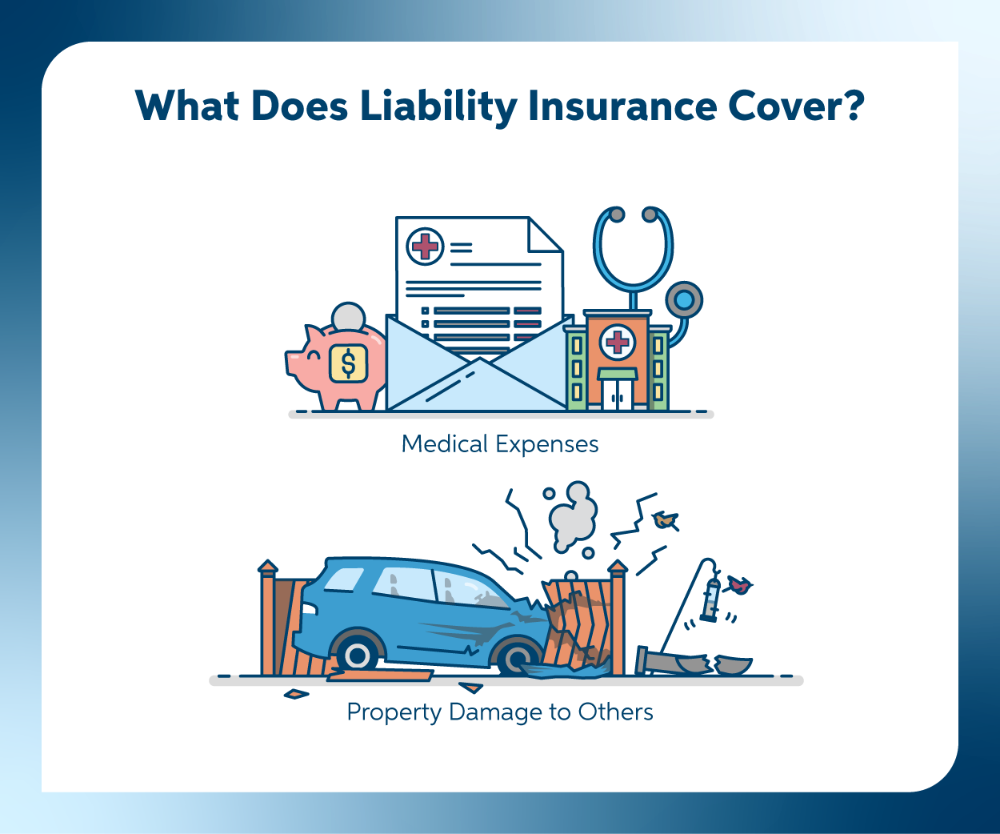

Liability car insurance is the most basic type of auto insurance and is legally required in most states across the United States. This type of coverage pays for damages or injuries that you cause to other people or their property if you are responsible for an accident.

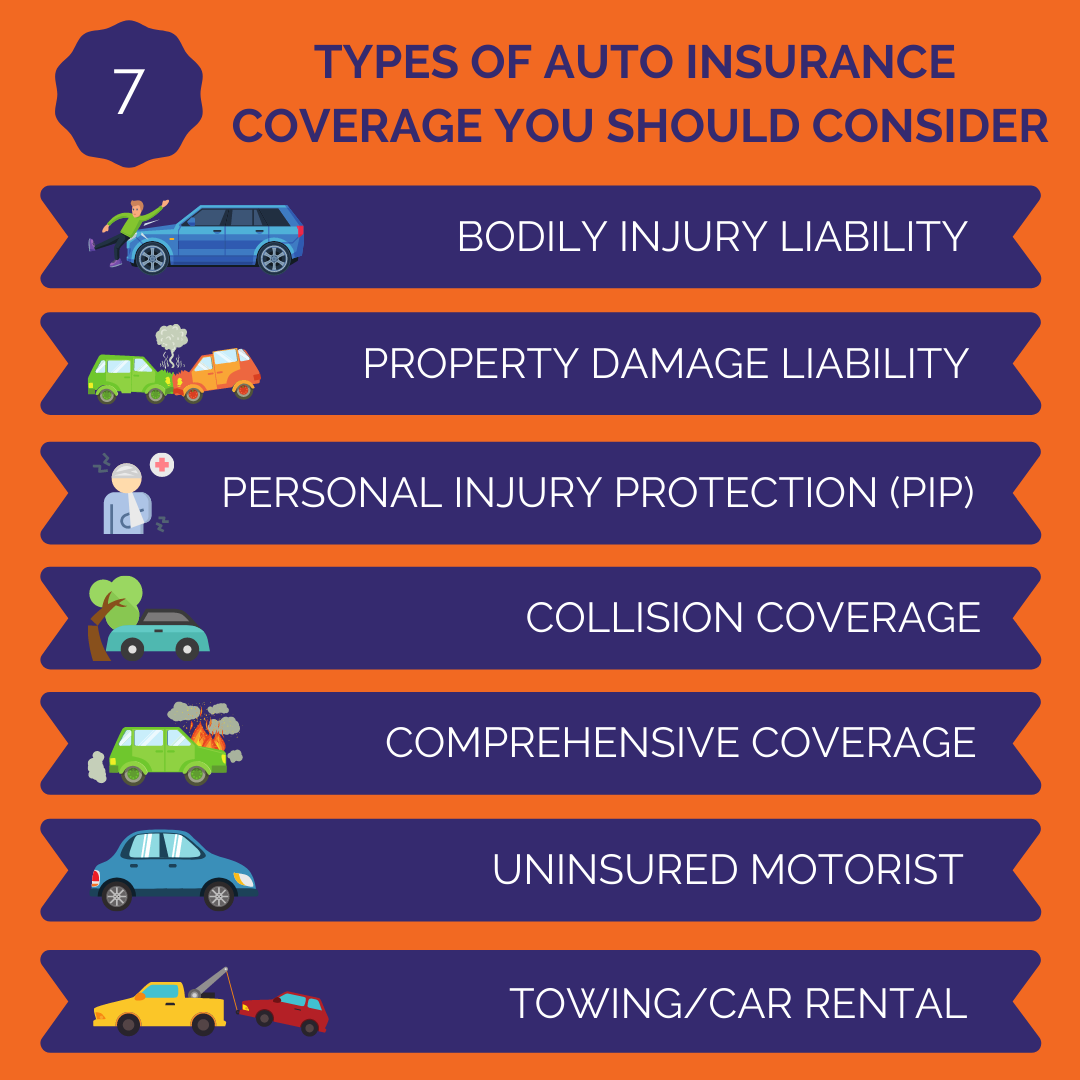

Liability insurance is typically divided into two main components.

Bodily Injury Liability

Bodily injury liability covers medical expenses, lost wages, and legal fees if you injure someone in a car accident. For example, if you cause a collision that results in injuries to another driver or passenger, this coverage will help pay for their hospital bills and treatment.

Property Damage Liability

Property damage liability pays for repairs or replacement if you damage someone else’s property. This could include another vehicle, a building, a fence, or any other property affected by the accident.

Liability insurance only protects other people and their property, not your own vehicle. If your car is damaged in an accident that you caused, liability insurance will not cover the repair costs.

What Is Full Coverage Car Insurance?

Full coverage car insurance is a broader insurance package that includes liability insurance along with additional protections. Although the term “full coverage” is commonly used, it is not a specific policy type. Instead, it generally refers to a combination of multiple coverage types that provide greater financial protection.

Full coverage typically includes the following components.

Liability Coverage

Like basic liability insurance, full coverage includes protection for damages and injuries you cause to other people.

Collision Coverage

Collision insurance pays for repairs to your vehicle if it is damaged in an accident with another car or object such as a tree, pole, or guardrail. This coverage applies regardless of who is at fault.

Comprehensive Coverage

Comprehensive insurance protects your car from non-collision events such as theft, vandalism, fire, natural disasters, falling objects, or animal collisions.

Together, these coverages provide much broader protection compared to liability insurance alone.

Key Differences Between Full Coverage and Liability Insurance

Understanding the main differences between these two insurance options helps drivers choose the right level of protection.

Coverage Scope

Liability insurance only covers damages and injuries to other people. Full coverage insurance protects both other people and your own vehicle.

Cost

Liability insurance is significantly cheaper because it offers limited protection. Full coverage policies cost more because they include collision and comprehensive protection.

Vehicle Protection

If your vehicle is damaged in an accident that you cause, liability insurance will not cover the repairs. Full coverage insurance will pay for repairs or replacement depending on the policy limits and deductible.

Loan or Lease Requirements

If you finance or lease a vehicle, lenders usually require full coverage insurance. This ensures the vehicle is protected until the loan is paid off.

Average Cost Comparison

The cost difference between liability insurance and full coverage insurance can be significant. In the United States, liability-only policies often cost much less than full coverage policies.

For example, a basic liability policy might cost around $600 to $900 per year, depending on the driver’s age, driving record, and location. Full coverage insurance can cost $1,500 to $2,500 per year or more because it includes additional protection.

Although full coverage is more expensive, it may save thousands of dollars if your vehicle is damaged or stolen.

When Liability Insurance May Be Enough

In some situations, liability insurance may be a reasonable option for drivers.

Older Vehicles

If your car is older and has a low market value, the cost of full coverage insurance might exceed the value of the vehicle itself. In this case, liability insurance could be a more cost-effective choice.

Budget Limitations

Drivers with limited budgets may choose liability insurance because it provides the minimum legal protection required to drive.

Secondary Vehicles

Some drivers choose liability coverage for older or secondary vehicles that are not used frequently.

When Full Coverage Insurance Is the Better Choice

Full coverage insurance may be a better option in several scenarios.

New or Expensive Vehicles

If your car is new or expensive, full coverage insurance protects your investment. Repairing or replacing a modern vehicle can cost thousands of dollars.

High Theft Areas

Drivers living in areas with high vehicle theft rates may benefit from comprehensive coverage, which protects against theft and vandalism.

Financing or Leasing

Most lenders require full coverage insurance until the car loan or lease is fully paid.

Peace of Mind

Full coverage provides more financial security and peace of mind because it protects against a wider range of risks.

Pros and Cons of Liability Insurance

Advantages

Lower monthly premiums

Meets the minimum legal requirement in most states

Simple and affordable coverage

Disadvantages

Does not cover damage to your own vehicle

Provides limited financial protection

May leave drivers responsible for costly repairs

Pros and Cons of Full Coverage Insurance

Advantages

Covers both your vehicle and other people’s property

Provides protection against theft, vandalism, and natural disasters

Often required for financed vehicles

Disadvantages

Higher insurance premiums

Requires paying a deductible for claims

May not be necessary for older vehicles

Tips for Choosing the Right Car Insurance

Selecting the right insurance coverage depends on several personal factors. Drivers should consider the value of their vehicle, their financial situation, and their risk tolerance.

Comparing quotes from multiple insurance providers is also essential. Different companies may offer different rates and discounts based on your driving history, location, and vehicle type.

Drivers should also review available discounts such as safe driver discounts, multi-policy discounts, and good student discounts, which can significantly reduce premiums.

Conclusion

Choosing between full coverage car insurance and liability insurance depends on your financial needs, vehicle value, and level of risk you are willing to accept. Liability insurance provides the minimum protection required by law and is the most affordable option. However, it does not cover damage to your own vehicle. Full coverage insurance offers broader protection by including collision and comprehensive coverage, making it the better choice for newer or high-value vehicles. By understanding the differences between these two insurance options and comparing multiple policies, drivers can select the coverage that provides the best balance between affordability and protection.